News & Publications

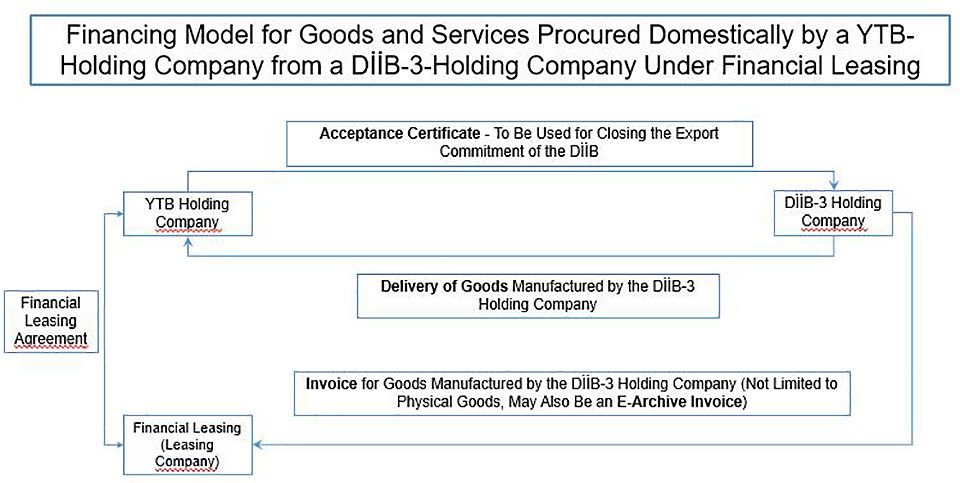

Procurement of Goods and Services by a YTB Holding Company from a DİİB-3 Holding Company Through Financial Leasing

The most significant amendment introduced by the Communiqué on Amendments to the Communiqué on Sales and Deliveries Deemed as Exports (Export: 2005/2), published in the Official Gazette on September 13, 2024, under the reference number (Export: 2024/3), is the facilitation of the procurement of goods and services covered by an Investment Incentive Certificate (“YTB”) [1] through financial leasing. This amendment allows companies holding a Certificate for Sales and Deliveries Deemed as Exports (“DİİB-3”) [2], which is used to fulfill export commitments, to manufacture and sell these goods and services.

Considering that the lists of goods and services specified in YTB annexes are categorized separately for domestic and international procurement, the goods and services to be procured under this amendment are expected to be listed under those designated for domestic procurement.

Additional explanations regarding this regulation, particularly concerning the procurement of goods and services under the financing model outlined below, are provided with respect to the document structure. These explanations are crucial both for YTB-holding companies and for DİİB-3-holding companies to fulfill their export commitments.

Significance of Documents Issued in Compliance with Export Incentive Regulations

Considering the workflow diagram above, the importance of the documents issued within the scope of export incentive regulations is outlined below:

Invoice

The invoice issued by the company holding the DİİB-3 may pertain to goods, services, or both. One critical point to consider is that the goods and services procured through leasing must align, both in terms of description and quantity, with those specified in the YTB annexed lists, which are categorized as domestic and international.

Since the invoice must be issued in the name of the financial leasing company while also ensuring the delivery of the invoiced goods/services to the YTB-holding company, it is essential that the invoice establishes a clear link between the parties involved. Accordingly, the invoice should include details of the YTB and the financial leasing agreement.

If the invoice is issued in printed form, it must include a statement indicating that the YTB-holding company has received the goods/services. If the invoice is issued as an electronic invoice, verification of receipt must be conducted electronically.

Acceptance Certificate

The Acceptance Certificate must contain the following information:

- Confirmation that the goods/services have been received by the YTB-holding company

- Financial leasing contract number

- YTB reference number

- Date and reference number of the invoice issued by the DİİB-3-holding company

The Acceptance Certificate, which is used to fulfill the export commitment of the DİİB-3-holding company, must include all the above details to ensure compliance.

Bibliography

- [1] Investment Incentive Certificate (“YTB”) (Yatırım Teşvik Belgesi) is a document that comprises the specifications of the investment and allows leveraging on the registered support elements as long as the investment has been realized in line with the set criteria.

- [2] Certificate for Sales and Deliveries Deemed as Exports (“DİİB-3”) (Dahilde İşleme İzin Belgesi) refers to the Documents issued pursuant to the Export 2005/2 Communiqué within the scope of the Inward Processing Regime for sales and deliveries considered as exports, in accordance with customs exemption regulations.

The above information reflects the general assessments of YılmazÜlker Attorney Partnership ("YılmazÜlker") regarding the subject matter and do not constitute legal opinion or legal consultancy services. Before taking any action based on the matters stated herein, it is recommended to seek professional legal advice by considering the specific circumstances of the case. YılmazÜlker shall not be held liable for any consequences arising from or in connection with the content of this document.

#YilmazUlker #InvestmentIncentive #TurkishLegislation #FinancialLeasing #Publication